Since the pandemic started, we have seen major imbalances to supply and demand in the global markets. Supply chain disruptions due to lockdowns and other regulations, restrictions in travel, trade and businesses shutting down while at the same time we saw a negative demand shock in air travel industries, restaurants, tourism, movie theaters, etc. Thus, it shouldn’t come to us as a surprise that we are seeing rapid price adjustments (especially for products that we use every day).

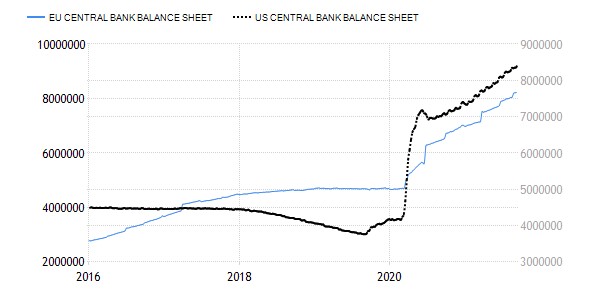

Furthermore, a huge increase in the money supply has seen the FED’s and ECB’s balance sheet increase dramatically.

Source: Tradingeconomics.

The ECB had expanded her own at around 54% of the Eurozone’s GDP during the summer. Government spending to GDP increased sharply both in the USA and in the Eurozone to stop falling aggregate demand, this of course led to huge deficits thus an explosion in public debt. There is also wide spread belief in the markets that central banks will continue to follow a relatively easy monetary policy combined with an extension of fiscal measures due to a slower recovery. Both in the EU and the USA inflation exceeded the targets set by the central banks with a risk of climbing even higher if action is not taken immediately.

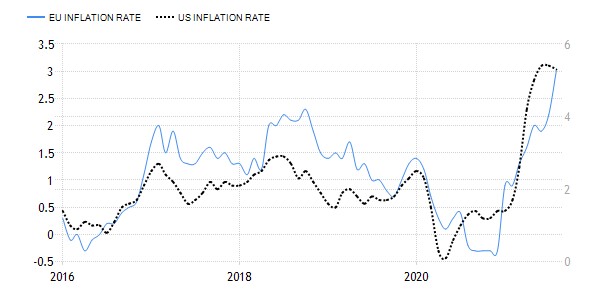

Source: Tradingeconomics.

Policy makers both in the USA and Europe have talked and warned about future inflation rates being higher than forecasts. Things get even more tricky when Jerome Powell is willing to tolerate an inflation target of higher than the traditional 2% for an unspecified amount of time. Since the ’08 crisis independence of central banks has withered yet their powers are greater than ever with no monetary rules being in place to keep things in check. Annual inflation of 3 or 4 or even 5% may seem low to some but as former FED chairman Paul Volcker has said: “Aiming for 2% inflation every year means that after decade prices are more than 25% higher and the price level doubles every generation. That is not price stability, yet they call it price stability.”

Almost 50 years ago in 1971, President Nixon imposed wage and price controls for the first time since WW2 with hopes of containing inflation. During the 1971 and 1974 the Wholesale Price index (WPI) increased at an annual rate of 12% and the CPI at a rate of 7.2% after the end of the Nixon program in 1974 inflation fell but in 1978 it saw a rise again this time under the Carter administration who on October 1978 announced a new set of voluntary wage and price control’s however only the huge rise in interest rates by FED chairman P. Volcker was capable of stopping inflation with the cost of a short run deep recession.

Before we discuss however the need for wage and price controls, we need to understand the causes of inflation. Increases in aggregate demand (via increased government spending) and aggregate expenditures (faster than the increase in goods and service) can happen only when the money supply is larger than the demand for it. With production not expanding in step with the monetary increase. Milton Friedman famously won a Nobel prize in economics for showing the correlation between excess money supply over output and the general increase in prices. “Inflation is always and everywhere a monetary phenomenon.”

Economists generally agree on very few things, but the economic case against price controls is one of them. The first consequences of the controls are shortages especially if the controls are kept for a long period of time causing widespread economic damage. There is a reason why Nobel winning economist F.A. Hayek described the free price system as a miracle because it works as a signal, providing information to both buyers and sellers of the scarcities of products in the marketplace, when prices are manipulated, these signals are also distorted, firms don’t have an incentive to increase supply due to lower profits with others getting out of production thus paving the way for the creation of black markets. Prices inform everyone about consumer needs, how much they are willing to pay for it, while at times of high uncertainty discouraging hoarding. The very existence of profits tends in the long run to bring prices down because they give incentives to the entrepreneurs to produce more of it which will increase supply and may even reduce costs due to economics of scale. On the other hand, price controls or anti-gouging laws discourage innovation and sometimes can lead to supplies of goods and services being directed to foreign markets where these controls don’t apply, the very basic economic law of supply and demand explains that if you artificially suppress rising prices, you will get less supply. Imperfections in the price system do not justify the need to control it by central planners.

Controls draw attention away from the real causes of inflation and give short term excuses for avoiding structural reforms in the economy. Fighting inflation is not an easy task, a tight monetary policy will lead to unemployment in the short term, cuts in government spending are needed and businesses that gave large wage increases due to inflation expectations would be in a bad situation. However, like most of our problems inflations is made in DC and in Brussels it is the FED and the ECB which are responsible for creating excessive money growth and there is no way of solving this issue unless this growth matches the output of the economy.

Economists agree that controls produce uncertainty, they prevent businesses from expanding operations and production. While they (controls) are able to put a short time freeze on prices, after the end of them inflation bursts up resulting in higher prices in the long run. As Eamonn Butler and Robert Schuettinger write in their book Forty Centuries of Wage and Price Controls: “If a historian were, to sum up what we have learned from the long history of wage and price controls, he would have to conclude that the only thing we learn from history is that we don’t learn from history.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}