Palantir Technologies (PLTR) has a fresh catalyst from Washington at a time when the stock is sitting in an important technical support area near key moving averages. Earlier this month, a Pentagon memo said the Defense Department plans to make Palantir’s Maven digital battle-management system a formal program of record by the end of the current fiscal year, a move that would place Maven on a more durable funding path and deepen its role inside the military’s operating stack.

Maven is used for battlefield awareness, intelligence analysis, targeting support, and decision-making, and future contracting is expected to shift under the Army.

The Army expanded the program with a $795 million contract modification in May 2025, and Palantir’s broader defense footprint continued to widen after that through a multiyear Army enterprise agreement worth up to $10 billion.

Related: Morgan Stanley has a stark message for investors in Palantir stocks

The Navy added another major win in December 2025 when it committed $448 million to Ship OS, a program built around Palantir software and AI adoption across the shipbuilding base. Taken together, those wins make the Pentagon story less about one contract and more about a company moving deeper into core defense systems.

Palantir by the numbers

- Q4 2025 revenue: $1.407 billion.

- Q4 2025 U.S. commercial revenue growth: 137% year over year.

- Full-year 2025 revenue: $4.475 billion.

- Q4 2025 GAAP net income: about $609 million.

- Year-end 2025 cash, cash equivalents, and short-term Treasuries: about $7.2 billion.

- Full-year 2026 revenue guidance: about $7.18 billion.

Source: Yahoo!Finance.

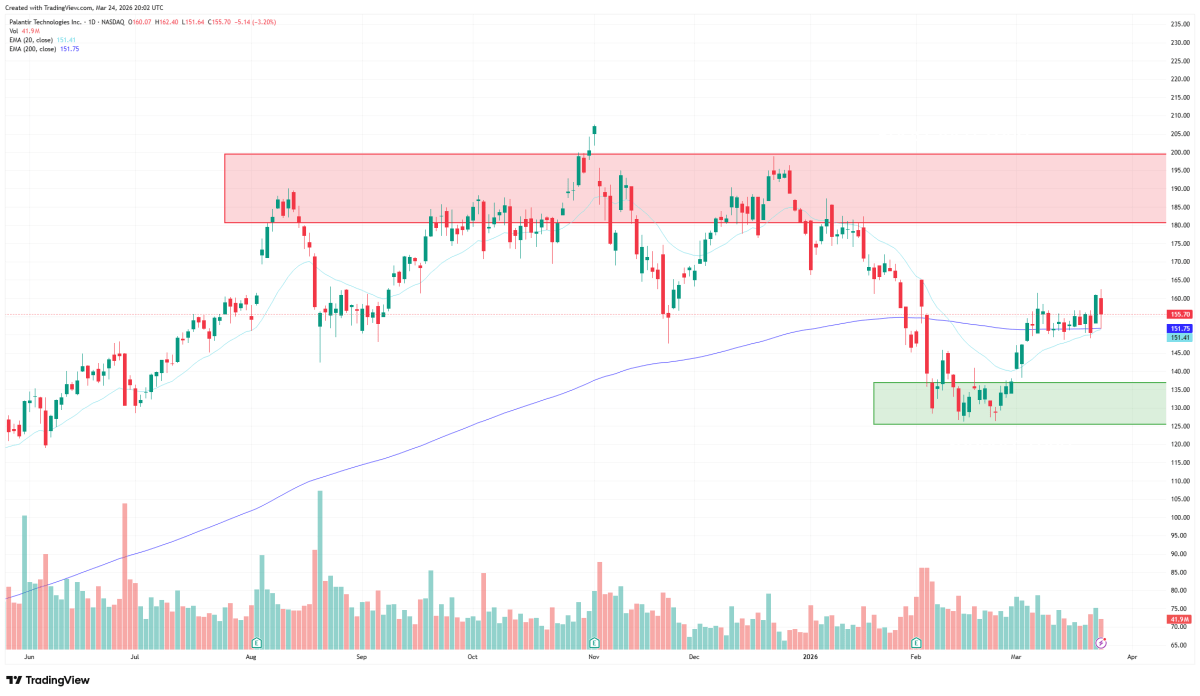

Palantir’s stock price tests key support at EMAs

The technical picture has improved, but it is not clean yet. Shares are trading near both the 20-day and 200-day exponential moving averages (EMA), trend lines commonly used by technical analysts as support levels

The 20-day EMA (light blue) is currently around $151.4, and the 200-day EMA (dark blue) is around $151.8. Both are sloping upward, which analysts consider constructive, and the short-term average is below but close to the long-term average, suggesting a bullish cross could develop if momentum continues.

At the same time, Palantir is still below a resistance zone that has repeatedly capped rallies in roughly the $180 to $200 range. Meanwhile, more support sits lower, in the $125 to $137 area, where buyers previously stepped in after the sharp selloff earlier this year. The setup appears to be a recovery in progress rather than a confirmed breakout.

What Palantir stock analysts think

UBS raised its price target to $200 from $180 and kept a Buy rating, and Piper Sandler kept an Overweight rating while lifting its target to $230 from $225 in early February, according to TheFly.

Rosenblatt raised its target to $200 from $150 in early March and maintained a Buy rating. On the more cautious side, Deutsche Bank raised its target to $200 from $160 but kept a Hold rating, arguing that the business is improving even if valuation still limits upside.

More Palantir

- Palantir is offering students a jaw-dropping $10,000 a month

- Palantir just got a headline-grabbing boost from the Iran war

- Veteran analyst drops eye-popping price target on Palantir stock

That split is probably the cleanest way to frame the stock right now. Palantir keeps adding evidence for the bull case through defense wins, accelerating growth, and profitability at scale. Bears are no longer making the simple argument that the business lacks momentum. The pushback is that the stock already reflects a lot of success and leaves less room for mistakes.

That is why the current setup matters. The Pentagon catalyst strengthens the fundamental story, and the chart is trying to improve at the same time. The next move in the stock will likely depend on whether that combination is enough to push Palantir through resistance instead of back into another rejection.

Related: Boeing inks Israel bomb deal worth up to $289 million